Futures Market: Overnight, LME copper opened at $9,763/mt, initially fluctuating upward to a high of $9,800/mt before fluctuating downward to a low of $9,729/mt. By the end of the session, the price center rose to a high level, closing at $9,679/mt, up 1.14%. Trading volume reached 18,000 lots, and open interest stood at 297,000 lots. Overnight, the most-traded SHFE copper 2504 contract opened at 79,800 yuan/mt, initially reaching a high of 79,870 yuan/mt before fluctuating downward to a low of 79,340 yuan/mt. After a slight rebound, it continued to pull back, closing at 79,530 yuan/mt, up 0.86%. Trading volume reached 34,000 lots, and open interest stood at 165,000 lots.

【SMM Copper Morning Brief】News: (1) US February CPI data fell short of expectations across the board, fueling market expectations for a US Fed interest rate cut in June. Traders increased their bets on at least two rate cuts within the year.

(2) According to market sources, due to tightening copper concentrate supply, spot copper concentrate TC/RCs continued to decline. Smelters under Tongling Nonferrous Metals Group have implemented production cuts, advanced maintenance with extended durations, and unscheduled maintenance to curb further deterioration in the spot copper concentrate market and safeguard the interests of domestic smelters.

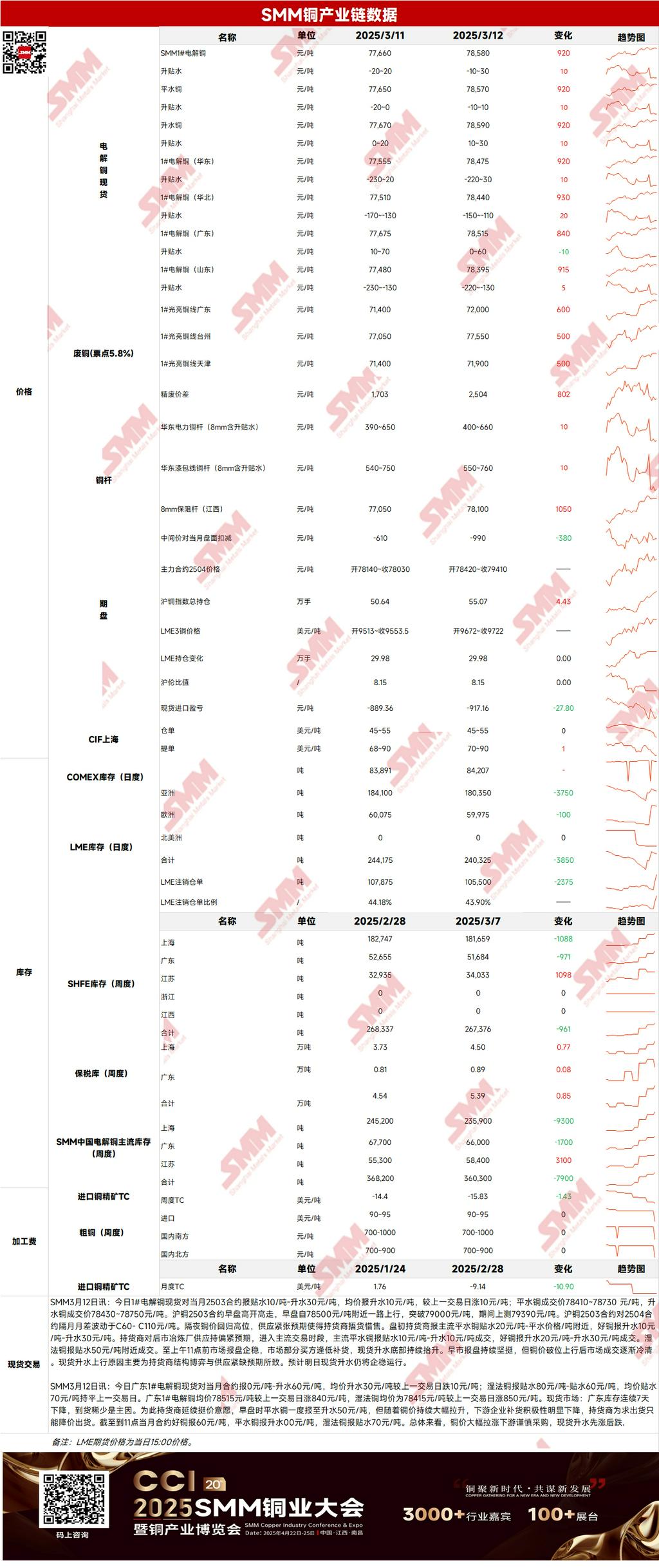

Spot Market: (1) Shanghai: On March 12, #1 copper cathode spot prices against the front-month 2503 contract were quoted at a discount of 10 yuan/mt to a premium of 30 yuan/mt, with an average premium of 10 yuan/mt, up 10 yuan/mt from the previous trading day. Early morning offers remained firm, but as copper prices broke upward, market transactions gradually turned sluggish. The rise in spot premiums was mainly driven by supplier structure dynamics and expectations of tight supply. Spot premiums are expected to remain stable today.

(2) Guangdong: On March 12, Guangdong #1 copper cathode spot prices against the front-month contract were quoted at parity to a premium of 60 yuan/mt, with an average premium of 30 yuan/mt, down 10 yuan/mt from the previous trading day. Overall, downstream purchasing remained cautious amid a sharp rise in copper prices, with spot premiums rising first and then falling.

(3) Imported Copper: On March 12, warrant prices ranged from $45 to $55/mt (QP March), with the average price unchanged from the previous trading day. B/L prices ranged from $70 to $90/mt (QP April), with the average price up $1/mt. EQ copper (CIF B/L) was quoted at $10 to $20/mt (QP March), with the average price unchanged. Quotes referenced cargoes arriving in mid-to-late March and early April. Yesterday, the SHFE/LME price ratio against the SHFE copper 2503 contract was around -900 yuan/mt. LME copper 3M-Mar was $14.37/mt, LME copper 3M-Apr was B$0.33/mt, and the March date to April date spread was around C$14.7/mt. The US dollar-denominated copper market remained sluggish yesterday, with limited activity in spot orders and overall weak trading sentiment.

(4) Secondary Copper: On March 12, secondary copper raw material prices rose by 600 yuan/mt MoM. Guangdong bare bright copper prices ranged from 71,900 to 72,100 yuan/mt, up 600 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 2,504 yuan/mt, up 801 yuan/mt MoM. The price difference between primary and scrap rods was 1,520 yuan/mt. According to the SMM survey, traders showed increased willingness to pick up goods. Due to the widening price difference between primary metal and scrap, many traders increased hedging activities, expecting copper prices to pull back later. However, terminal wire and cable enterprises remained cautious and adopted a wait-and-see approach.

(5) Inventory: On March 12, LME copper cathode inventories decreased by 3,850 mt to 240,325 mt. SHFE warrant inventories decreased by 2,352 mt to 149,351 mt.

Prices: Macro side, US February CPI data fell short of expectations across the board, fueling market expectations for a US Fed interest rate cut in June. Traders increased their bets on at least two rate cuts within the year. The US dollar index hovered near a five-month low. Combined with market digestion of the US-EU tariff dispute and potential Russia-Ukraine ceasefire, the macro environment was overall supportive of copper prices. Fundamentals side, supply side, copper prices at high levels led suppliers to expect tight smelter supply, resulting in strong sentiment to hold back cargoes, limiting market circulation. Demand side, downstream enterprises showed cautious purchase willingness amid sharply rising copper prices, mainly purchasing as needed. Overall market transactions were sluggish, with sellers and buyers in a stalemate. Price-wise, copper prices are currently driven largely by macro sentiment. However, uncertainties surrounding Trump's tariff remarks have heightened market caution. Copper prices are expected to fluctuate at highs today.

》Click to View SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided is for reference only and does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】